Tommy Lee Walker - stock.adobe.c

Data dive: UK government’s 2030 datacentre capacity targets look shaky

We look at UK datacentre capacity – current and projected – and find DSIT’s 2030 target for 6GW of AI-capable capacity is currently out of reach, unless operators get a move on

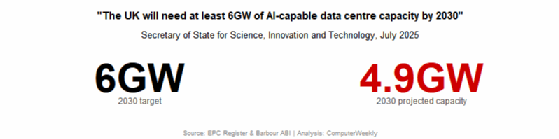

In July 2025, UK secretary of state for science, innovation and technology Peter Kyle said: “We forecast that the UK will need at least 6GW of AI [artificial intelligence]-capable datacentre capacity by 2030.”

As things stand, that target will likely not be met, with UK datacentre capacity on course to total 4.9GW by 2030, given the current planning status of many projects.

Current UK datacentre capacity is around 1.6GW. If we assume a big chunk of that is not “AI-capable”, then 6GW of “AI-capable datacentre capacity by 2030” looks a way off.

That figure – 4.9GW by 2030 – comes from the likely completion of datacentre projects that currently have planning approval. It is based on research by Computer Weekly, with data from construction pipeline trackers Barbour ABI, and for current operational datacentres is based on government electricity performance certificate data.

In this article, we look at currently operational datacentre capacity in the UK and the likely projected pipeline for the coming years. We break that down by approved and unapproved capacity in terms of planning applications.

We further look at the regional trends: where datacentres are now and where they will be built in the next decade in the UK. In future articles, we’ll take a closer look at the government’s plans for AI datacentre capacity and how their targets could be fulfilled.

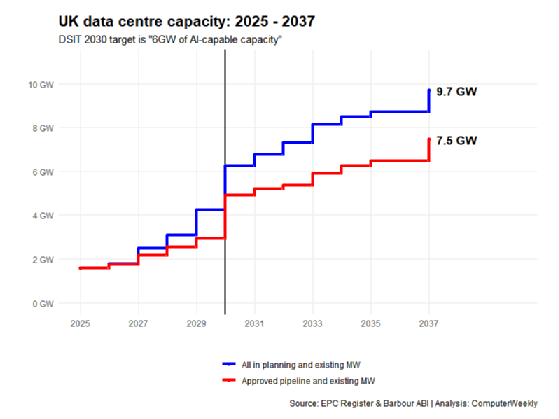

Can the pipeline get to 6GW by 2030?

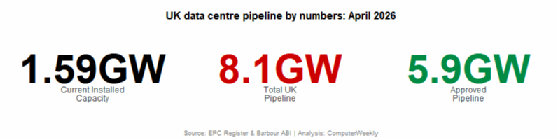

According to the data, the UK has about 1.59GW of currently installed datacentre capacity across just under 190 sites.

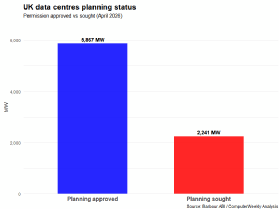

If we add existing capacity to that which is planned to be completed by 2030 and which has planning consent, we get 4.9GW.

Total pipeline, however, including projects that don’t yet have planning consent, is 8.1GW. The total of unapproved projects planned to be completed by 2030 is 6.2GW.

There is just about enough in the pipeline to achieve 6GW by 2030. But that would require a rash of planning applications to go through in time to start construction in 2027, assuming a three-year build period.

Having said all that, there must be some doubts about how much of that 6GW would be classed as “AI-capable” datacentres.

How much capacity will be AI-capable?

Many datacentres in the existing capacity base are old and relatively small.

About 14% (27/120MW) of 190 operational datacentres are at least 10 years old. That’s not to say they won’t have been upgraded, but increasing power and cooling requirements over time mean they need more of both to support processing with each upgrade, and the number of racks that can be hosted in the same physical footprint decreases. Meanwhile, 42% (80/600MW) of existing datacentres are more than six years old.

Also, most datacentres in the currently installed capacity base are very small by current standards. Based on estimates in the data (see below), most (77%, or 147 of the 190) have a capacity of less than 10MW.

Current AI rack power draw maxes out at about 100kW. AI processing also needs liquid cooling. Power draw of 1MW per rack is only two to three years away, according to the Nvidia graphics processing unit (GPU) roadmap.

That’s why 18 out of 190 currently proposed datacentres – including the giants in the government’s AI growth zones – account for 68% of all planned capacity by 2037. That is 5.5GW of a total pipeline of 8.1GW.

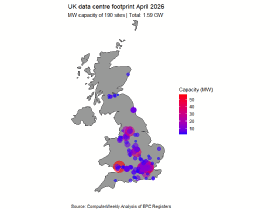

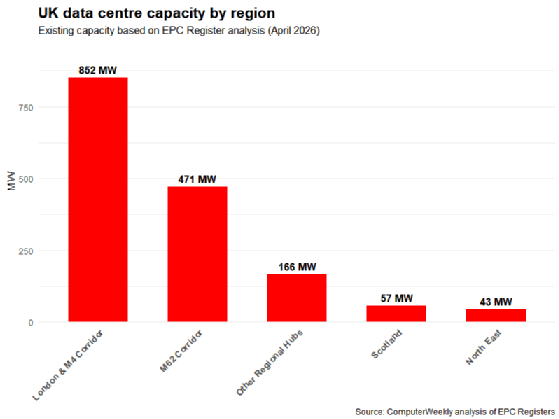

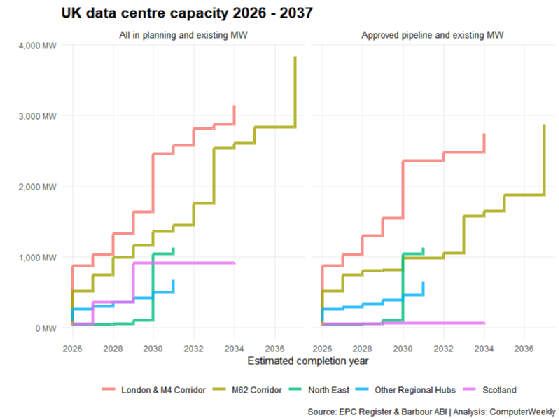

The bulk of operational capacity is centred on London and the M4 corridor right now, with just over 850MW of the 1.59GW total in that region. The M62 corridor – taking in Manchester, Liverpool, Leeds and Hull – comes next, with 471MW installed. Scotland and the north-east of England have around 50MW of installed capacity each.

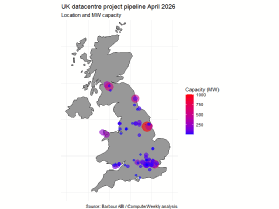

While it is very difficult to get precise megawatt capacities for datacentres, we can be sure there isn’t much in the way of more than 100MW in any one datacentre in the UK right now. That’s all set to change, with projects planned of several hundred megawatts – 600MW at East Havering, 550MW at Ravenscraig, 500MW at Blyth, for example – and 1GW (gigawatt) at Elsham in North Lincolnshire.

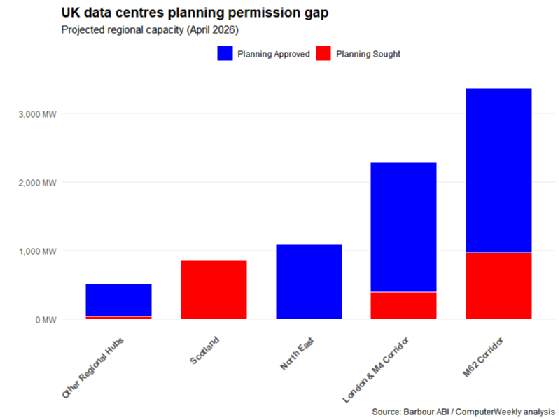

While the most rapid datacentre development has been centred on the south-east so far, that’s set to change, with the centre of gravity shifting north. The M62 corridor has the biggest pipeline, with 3.3GW projected. London and the M4 corridor comes quite a distance behind with about 2.2GW. Having said that, when we strip out projects that haven’t yet got planning consent, the M62 region drops back to about 2.2GW and London to less than 2GW.

As we’ve seen, however, that level of building will increase the UK’s datacentre capacity by around four times, much of which will have come on stream by the first year or two of the next decade.

Perhaps worrying for Scotland, however, is that the vast bulk of planned megawatts there does not yet have planning consent. However, there are only four datacentres planned in Scotland in the Barbour ABI data, and two of them account for more than 99% of that (see chart: UK datacentres: Project scale distribution).

Both projects are in the public consultation phase, with the largest of these – the 550MW former Ravenscraig steelworks site – being considered as a government-backed AI growth zone.

By 2034, London and the M4 corridor will still be home to the most UK datacentre capacity, but with the M62 region catching up. In fact, as things stand in terms of approvals, the Hull-Manchester-North Wales axis is set to overhaul the south-east by the mid-2030s.

If the chart (UK datacentre capacity 2026-2037) shows the M62 lagging a little, that is because it doesn’t show the staged addition of capacity at Elsham Tech Park as it builds towards its full 1GW by 2037.

Where the data comes from

Barbour ABI collates planning application data from UK local authorities for construction industry customers. We can use it to see the datacentre pipeline. While the data is extremely useful, planning application information provides challenges for those who want to track datacentre projects.

Because there is no requirement in planning applications to explicitly label a project as a datacentre, we estimated megawatt capacity for many sites listed based on the relationship of floor area and megawatts in a sample where both values are known.

We built estimates of existing installed datacentre capacity by tracking down likely datacentres in UK government energy performance certificates registers (including for Scotland).

Datacentres use a lot of electricity, so we filtered for a “primary energy value” of more than 1,000kWh per square metre per year – three to five times the standard industrial average – and cross-referenced that with a range of characteristics that included floor area, main heating fuel (to rule out gas use in mostly non-office buildings) and known keywords found in descriptions of datacentres.

That provided 190 likely existing datacentre sites and allowed an estimation of megawatt capacity.

Any megawatt figures are likely to be an underestimate as, over time, the megawatt draw of graphics processing units (GPUs) increases for the same physical footprint.

Read more about datacentres

- Hit the north! UK datacentre focus shifts to M62 and points north: Barbour ABI data shows 8GW of total datacentre pipeline with most big projects in the north and Scotland, while London and the M4 corridor are about 25% of projected capacity.

- Power supply issues flagged as major growth inhibitor of European datacentre market: The latest report into trends across the European datacentre market shines a light on how power supply issues are affecting growth.

Read more on IT outsourcing

-

![]()

IDCA warns of ‘delay tax’ as AI datacentre power surges 50%

By: Antony Adshead

-

![]()

SNP council backs datacentre halt and creates Burnham dilemma

By: Antony Adshead

-

![]()

nLighten CEO Dawn Childs on edge datacentres and sovereignty

By: Antony Adshead

-

![]()

AI’s next compute layer is likely to come from outside Silicon Valley